The man on the other end wanted to sell his small Iowa farm. And, of course, he wanted to sell it for a good profit. And then he wanted to use that money to buy another, larger farm.

Good idea!

But he didn’t want to pay any capital gains taxes on the land that he was selling.

Another good idea, right? I mean who does want to pay taxes?

Of course, he may have to pay taxes. We all do. Unless that is, we employ a process called the 1031-tax deferred exchange.

What is a 1031-tax deferred exchange? (or just 1031-tax exchange)

By using 1031 tax exchange, a person can “defer” the gains on the sale of real property into another piece of real property.

Any real property into any other real property. This means you can exchange a farm for another farm, a home, or maybe a commercial building, if desired, for example.

Say for instance that you purchased a 40- Iowa parcel of land ten years ago for $60,000. And, suppose, that right now you have a buyer that is ready to hand over $90,000 for that parcel of Iowa land.

What happens to the $30,000 gain?

In a normal transaction that gain is taxable and in this case would be considered a long-term capital gain (since it was held for at least one year). But by employing the process of the 1031- tax exchange, you would not have to pay any gain on that $30,000 (at least, not at the time of the sale).

The $30,000 gain would simply be rolled into the purchase price of another, usually larger, and more expensive property. Perhaps you found an 80-acre parcel down the road for $160,000 that you’d like to buy, for instance.

Well, now, if you carry out a 1031-tax exchange, you have most are all of the down payment necessary to purchase that 80-acre farm!

The good part is that you can use the full power of the gain instead of getting slammed with paying taxes on it.

This lets you build up to bigger and larger parcels of land much, much, faster and with less out-of-pocket expense than you ever could otherwise!

So, that entire capital gain, usually, transfers into another “replacement” property right after you sell. You don’t, normally, put any of it in your pocket but it does go right into an investment that is typically more expensive than the one you previously had. This is the basis of the process – the 1031-tax exchange process lets you carry gains with you as you step up to more expensive properties.

It’s not hard to see that doing this not only helps save you tons of tax money but it also helps you build up a bigger and healthier looking real estate portfolio over time (whether that was your goal of not).

Some people seem scared or intimated of the process or they think it is something new and “tricky”.

The 1031-tax exchange is used and has been used, by thousands of experienced real estate investors every year as a means to help create wealth and as a means to build up to bigger and better parcels of land. And it can and does do that! It is not a new or secret process.

How to go about using a 1031-tax exchange.

The first thing to realize is that doing a tax exchange, while simple in concept, is still rather complex.

There are lots of rules and stipulations that must be followed to the letter for this to work.

But, rest easy, a good real estate attorney will handle all of this for you. And you do need one if you are going to do a 1031-tax exchange.

In general, the seller of a property should establish if he/she wishes to carry out an exchange before they decide to sell.

An attorney will set up the required documents for the 1031 tax exchange process to carry out legally and accurately.

When you sell your property for a profit, you then have 45-days to find a suitable replacement property. This is usually a more expensive and, thus, often is also a larger property that you will move the capital gain of the sale of the relinquished, property into.

Once you’ve identified a replacement property, you then have 6-months to close on that property.

Again, you will want a good real estate attorney who is familiar with 1031-exchange laws to carry this out for you! (They are not hard to find via Google or the good old yellow pages!)

A neutral, third-party, intermediary actually holds the money from the gain of the relinquished property in a trust account until the closing day of the replacement property (known as a “safe harbor”).

An important component of the laws around this is that the seller of the relinquished property never really touches the profits!

Most of the time all of the profits from the sale of the relinquished property are then put right back into a replacement property.

One can keep some of the profits if they desire, but those profits would be taxable (known as “taxable boot money”). Again, the 1031-tax exchange rules are strict and the procedures must be carried out exactly as prescribed.

But don’t let that scare you, a good attorney will handle this for you!

You don’t really need to do anything yourself, as a seller, but to concentrate on selling your property. And then on finding a suitable replacement for your profits to go into.

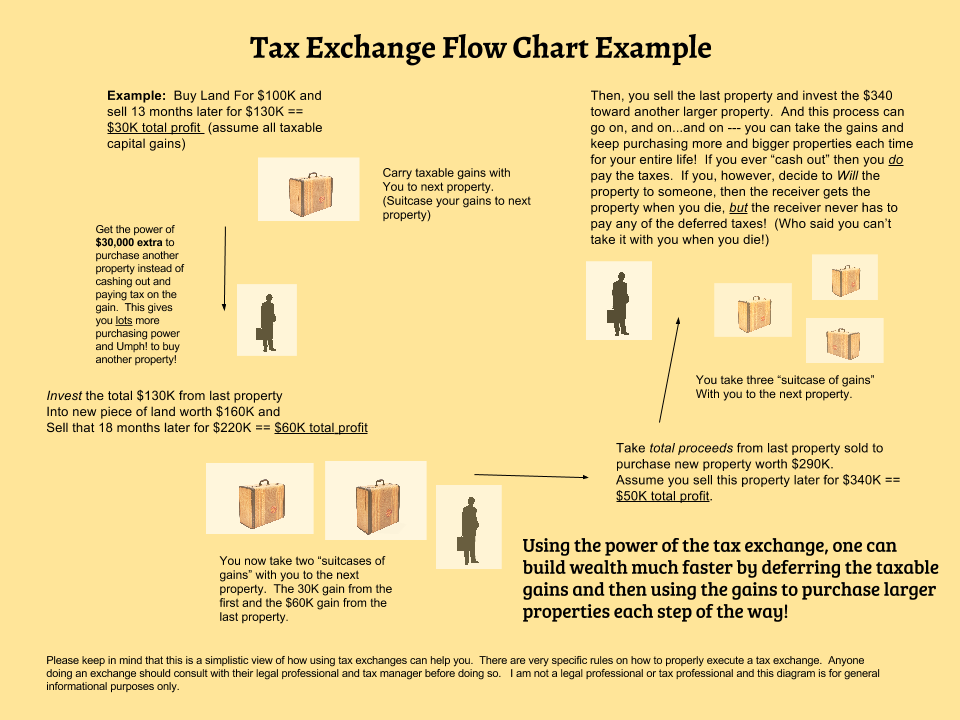

Flow chart showing the process and power of using a 1031-tax deferred exchange.

An interesting thing to note is that you can carry on this 1031 exchange process your whole life – that is, you can buy and sell, buy and sell, buy and sell, each time making profits that roll into the next using the 1031 tax exchange process.

Each time you do this you are carrying all of the profits from one property into the next – helping you to build more and more acres of land each time you carry it out.

This sort of multiplier effect of being able to use all of the profits, instead of paying huge taxes on each sale, each time you “reload” to get more land is huge!

The 1031 tax exchange process really lets you build up allot of valuable land in the quickest and cheapest way possible. Simply put, you get a huge break each time you buy because you aren’t paying taxes on the profits of the previous sale – the profits all go straight into your new replacement property. This happens each and every time you do this – for as long as you want.

But why do they call it a 1031 deferred tax exchange if you never have to pay taxes on the land that you continue to buy?

Well, at some point, when you decide to sell your final piece of land later in life and want to take the profits with you to live the good life in Hawaii, then you would need to pay the taxes on the profits of the sale.

But maybe instead of taking the profits out of your final parcel of land and moving to Hawaii, you simply decide to “will” the assets that you acquired using the 1031 process to your heirs.

Then – when you die – your property all gets transferred to those chosen and they do not have to pay any of the taxes that you deferred along the way.

No kidding!

They would pay taxes on the property that you gave to them should they elect to sell but they do not have to pay all the back tax-deferred gains that you used to get there!

They would just be taxed on any gain from the sale of the property that is over and above the then appraised value of the property.

There you have it: a quick overview of the 1031-tax exchange process. Keep in mind that I am not an attorney and that this information is just meant as general guidance based on my understanding of the current tax code. You should always seek the representation of a qualified real estate attorney and/or other tax professional when doing a 1031-tax deferred exchange.

When pondering Iowa fence law, my mind drifts back to a client and I busting through some thick nasty cover one sultry day a few July’s back, swatting flies as we walked, and checking out the fenceline on a 120-acre farm along the Des Moines river, in Iowa.

“This fence is pretty rough,” he said, as we paused at the top of a little ravine.

Your right this fence-line can barely be called a fence-line, that’s for sure. I answered back.

From the looks of things, no livestock had been on either side of that fence in a long, long, time.

And it appeared that neither landowner really cared about the condition of the fence anymore since neither seemed to have livestock to contain.

“What are my obligations for the fence,” my client asked. “Am I required to make the fence better or build a new fence if I buy the place”?

Perhaps…..

A look into The Iowa fence law code:

(The Iowa fence law code is very old and some of it dates back to the late 1800’s and earlier!)

If you are an Iowa landowner then you may already be familiar with Iowa fence law.

The law is rather out-dated and there are plenty of folks who disagree with some or all of it (especially those that don’t own livestock, it seems.)

The law states that existing border fences be maintained by both landowners and that the expense shared by both adjacent landowners.

Additionally, if there is no border fencing, and if one owner decides to have one, then that person can demand, by written request, the adjacent landowner to build a legal fence.

“Respective owners of adjoining tracts of land shall upon written request of either owner be compelled to erect and maintain partition fences, or contribute thereto, and keep the same in good repair throughout the year.” (a)

Who Pays for the Fence?

In determining how to apportion fence responsibilities under the statute, many landowners have traditionally applied the right-hand rule: two adjoining property owners, facing each other at the center of the fence along their shared property boundary, each agree to build the right half from the center of the property to the end of the property line. While this is an acceptable practice, it is not based in statutory or case law. Thus, it is not a required method of allocation. ( Iowa Fence Requirements: A Legal Review By Kristine A. Tidgreni July 27, 2016 )

Let’s go back to the question of my client.

Does he need to make that poor, below-code, fence-line better if he buys the land? Even though neither side owns or runs livestock?

He may need to make that border fence-line better – it all depends upon what the adjacent landowner desires.

For one thing, if the adjacent landowner requests a fence then it needs to be a legal fence. (If neither neighbor cares about having a fence then there is no statutory requirement to have one).

A legal fence means it must meet the minimum criteria the established by the Iowa code.

What if the adjacent landowner desires, an even better fence than the Iowa fence law code has established as the minimum allowance for a legal fence? The Iowa fence law provides that all partition fences may be made tight by the party desiring it, and when that party’s portion is so completed, the adjoining landowner must follow suit. ( Iowa Code § 359A.19.) A tight fence must be “securely fastened to good substantial posts, set firmly in the ground, not more than 20 feet apart.” (Iowa Code § 359A.20 )

359A.20 TIGHT FENCE:

All tight partition fences shall consist of:

1. Not less than twenty-six inches of substantial woven wire on

the bottom, with three strands of barbed wire with not less than

thirty-six barbs of at least two points to the rod, on top, the top

wire to be not less than forty-eight inches, nor more than fifty-four

inches high. 2. Good substantial woven wire not less than forty-eight inches

nor more than fifty-four inches high with one barbed wire of not less

than thirty-six barbs of two points to the rod, not more than four

inches above said woven wire. 3. Any other kind of fence which the fence viewers consider to be

equivalent to a tight partition fence or which meets standards

established by the department of agriculture and land stewardship by

rule as equivalent to a tight partition fence.

You may wonder if you have a duty to build and or to maintain a boundary partisan fence if you do not own livestock?

It would seem that the answer would be no.

But the real and legal answer, it seems, is yes.

In Iowa, landowners with livestock have a duty, by law, to fence their livestock in so that they don’t run at large. (lawful duty to fence livestock in)

However, adjacent landowners who do not own livestock are obligated by law to maintain their portion of any boundary partisan fence. (lawful obligation to keep livestock out)

This means that even if you do not own livestock and you do not maintain a sufficient and legal partition fence then you have little to no recourse for any possible damages that may be caused by livestock escaping onto your land.

The livestock owner would likely not be held responsible for damages if you do not maintain a legal partisan fence to keep his livestock out.

The law is pretty crazy in this regard if you ask me. But that is the way it is.

But that is the way it is.

It is sort of like saying, I’ve got this pit-bull here in my yard on this leash.

But he is big and mean and nasty and he may break that thing and dash off. If he comes into your yard and mauls you, I can’t be held responsible because you didn’t put up an appropriate barrier to stop him.

I realize that sounds like a silly and extreme example but it is based on the same logic as the Iowa fence code is using in regard to livestock.

What do you think?

The Iowa fence law code does establish a nice base point at which boundary line disputes and rights of ownership can be corrected and maintained.

Disputes between neighbors regarding boundary fencing are resolved by fence viewers who are township trustees – either 3 or 5 registered voters of the township – that have been given special power to resolve fence-line controversies. They do not have the authority, however, to resolve legal boundary issues.

Property Ownership

There are ways in which property ownership rights can be established and transferred based simply upon where the partisan fence is located.

If a boundary fence exists and both sides don’t dispute it’s location for a period of at least 10 years, then that it becomes the legal boundary (boundary by Acquaintance). This is important because even though a boundary fence exists this does not mean it is on the real legal boundary or that it is on the exact location that a survey of the land would reveal. But after ten years, if neither landowner disputes the location of the partition fencing, then that becomes the legal border regardless (Iowa Code § 650.6)

This important for landowners to realize because often certain sections of border fencing is placed for convenience.

Fencing by convenience is not uncommon at all, and in fact, is done all the time, especially on rough and rugged terrain.

This is done to make it easier get around something when fencing off the border – perhaps the real line is close to the edge of a rock bluff or goes across a creek with big, steep hillside, for example.

In these cases, a landowner may place fencing just off to the edge of these places or slightly off and around the edge of these areas to more conveniently run the fence and, thus, dodge the obstacle.

If you are a landowner and have any questions regarding your land borders, I suggest going to the courthouse and looking at your plat-of-land. (county auditor).

Again, is not uncommon to have at least some portion of a fence-line, to be run by convenience, especially on large or “rugged” farms. If you find such to be the case on your farm, you should notify your neighbor right away, in writing, that you have knowledge of the real border in those areas and that the partition fence is not on it.

The are other ways ownership rights can be dictated and transferred by way of Iowa fence law code.

Something similar to Easement by Acquaintance is Easement by Prescription

With Easement By Prescription, both owners have knowledge that a border fence exists in the wrong area but they continue to use it as though it is placed correctly. If both sides continue to use the borders as the “real border” for a period of 10 years or more, then ownership rights can transer by means of easement by prescription. (When a landowner “uses another’s land under a claim of right or color of title, openly, notoriously, continuously, and hostilely for ten years or more” an easement by prescription is created. Iowa Code § 564.1.)

Adverse Possession:

Finally, misplaced fences could result in land acquired via “adverse possession.” Adverse possession is a similar doctrine to an easement by prescription, however adverse possession is obtained by occupying the land, not simply using it. (Iowa Code § 564.1.)

This covers some of the basics regarding Iowa fence law to get more details you should download

Iowa Fence Requirements: A Legal Review By Kristine A. Tidgreni July 27, 2016 (button at the bottom of this post)

Something fishy with Iowa fence law:

Sometimes a partisan fence runs right through the middle of a pond or lake.

In Iowa, landowners own the bottom of any lake or pond bed that sits on their land. In certain instances, the boundaries between adjacent landowners may run through a portion of a lake or pond.

Can a landowner put up a fence that runs through a lake or pond and on their property border, and fence other’s out?

Yes.

However, many owners choose to make different agreements that allow all owners of a shared lake to enjoy the whole water source. (b)

Credits: a: Gravert v. Nebergall, 539 N.W.2d 1184 (Iowa 1995). b: Fence Feuds: A Two-Sided Story posted by Shannon Holmberg | Jul 16, 2015

Maybe it’s a solid 100, 150, or even 200 acres. Maybe it’s just 5 acres. Maybe you have a farm with sections of timber scattered about. (as is, most commonly the case).

Are you tired of paying real estate taxes on land? (Dumb question right?)

We’ll you don’t have to pay taxes on Iowa forestland acres!

Really?

Yes, you heard me correct.

If you do own some Iowa forestland and don’t want to pay taxes then, of course, you can’t just stop paying your real estate taxes.

But, in general, the rules are minimal and to many Iowa landowners the benefit of not having to pay real estate taxes on their forestland acres far outweigh the rules and stipulations that must be followed to reap the tax saving’s benefit.

To sign up, go to the county assessor’s office in the county in which you own the land. Take a map of your property with you and circle all the areas you would like to enroll in the Iowa Forest Reserve Program.

Here are some of the basic criteria:

Must be at least 2 contiguous acres.

Must be at least 200 trees per acre (forestland), or 70 trees per acre (fruit trees).

must keep livestock out of the area.

There are some other minor stipulations as well regarding the Iowa Forest Reserve Program be sure to check those out on the link page above. (from the Iowa DNR)

Iowa Wildlife Habitat Services is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for us to earn fees by linking to Amazon.com and affiliated sites. We fully believe in and have used all the products that we provide links to. However, we care about you! So, please do not click on these links and do not purchase any items if you feel these products will not help you. We receive no sponsorship dollars and buy these items ourselves and only provide links to items that we think will help you!